Experiences about opening data in private sector

Experiences about opening data in private sector

Ⅰ. Introduction

Open data is the idea that data should be available freely for everyone to use and republish without restrictions from copyright, patents or other mechanisms of control. The concept of open data is not new; but a formalized definition is relatively new, and The Open Definition gives full details on the requirements for open data and content as follows:

Availability and access: the data must be available as a whole with no more than a reasonable reproduction cost, preferably by downloading over the internet. The data must also be available in a convenient and modifiable form.

Reuse and redistribution: the data must be provided under terms that permit reuse and redistribution including the intermixing with other datasets. The data shall be machine-readable.

Universal participation: everyone must be able to use, reuse and redistribute the data— which by means there should be no discrimination against fields of endeavor or against persons or groups. For example, “non-commercial” restrictions that would prevent “commercial” use, or restrictions of use for certain purposes are not allowed.

In order to be in tune with international developmental trends, Taiwan passed an executive resolution in favor of promoting Open Government Data in November 2012. Through the release of government data, open data has grown significantly in Taiwan and Taiwan has come out on top among 122 countries and areas in the 2015 and 2016 Global Open Data Index[1].

The result represented a major leap for Taiwan, however, progress is still to be made as most of the data are from the Government, and data from other territories, especially from private sector can rarely be seen. It is a pity that data from private sector has not being properly utilized and true value of such data still need to be revealed. The following research will place emphasis to enhance the value of private data and the strategies of boosting private sector to open their own data.

Ⅱ. Why open private data

With the trend of Open Government Data recent years, countries are now starting to realize that Open Government Data is improving transparency, creating opportunities for social and commercial innovation, and opening the door to better engagement with citizens. But open data is not limited to Open Government Data. In fact, the private sector not only interacts with government data, but also produces a massive amount of data, much of which in need of utilized.

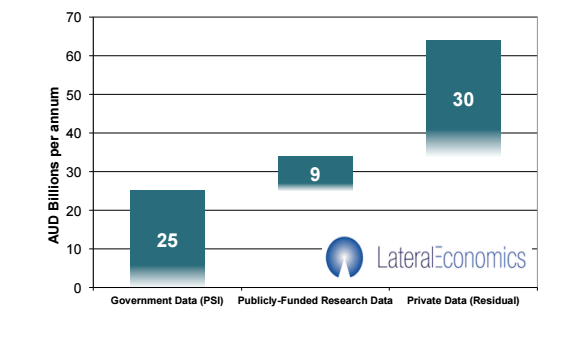

According to the G20 open data policy agenda made in 2014, the potential economic value of open data for Australia is up to AUD 64 billion per annum, and the potential value of open data from private sector is around AUD 34 billion per annum.

Figure 1 Value of open data for Australia (AUD billion per annum)

.png)

Source: McKinsey Global Institute

The purpose for opening data held by private entities and corporations is rooted in a broad recognition that private data has the potential to foster much public good. Openness of data for companies can translate into more efficient internal governance frameworks, enhanced feedback from workers and employees, improved traceability of supply chains, accountability to end consumers, and with better service and product delivery. Open Private Data is thus a true win-win for all with benefiting not only the governance but environmental and social gains.

At the same time, a variety of constraints, notably privacy and security, but also proprietary interests and data protectionism on the part of some companies—hold back this potential.

Ⅲ. The cases of Open Private Data

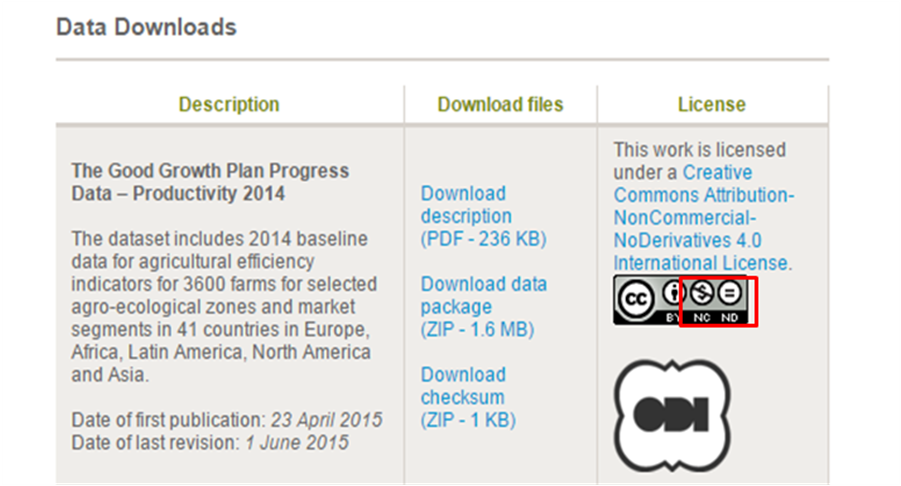

Syngenta AG, a global Swiss agribusiness that produces agrochemicals and seeds, has established a solid foundation for reporting on progress that relies on independent data collection and validation, assurance by 3rd party assurance providers, and endorsement from its implementing partners. Through the website, Syngenta AG has shared their datasets for agricultural with efficiency indicators for 3600 farms for selected agro-ecological zones and market segments in 42 countries in Europe, Africa, Latin America, North America and Asia. Such datasets are precious but Syngenta AG share them for free only with a Non-Commercial license which means users may copy and redistribute the material in any medium or format freely but may not use the material for commercial purposes.

Figure 2 Description and License for Open data of Syngenta AG

Source: http://www.syngenta.com

Tokyo Metro is a rapid transit system in Tokyo, Japan has released information such as train location and delay times for all lines as open data. The company held an Open Data Utilization Competition from 12 September to 17 November, 2014 to promote development of an app using this data and continues to provide the data even after the competition ended. However, many restrictions such as non-commercial use, or app can only be used for Tokyo Metro lines has weakened the efficiency of open data, it is still valued as an initial step of open private data.

Figure 3 DM of Tokyo Metro Open data Contest

Source: https://developer.tokyometroapp.jp/

Ⅳ. How to enhance Open Private Data

Open Private Data is totally different from Open Government Data since “motivation” is vital for private institutions to release their own data. Unlike the government data can be disclosed and free to use via administrative order or legislation, all of the data controlled by private institutions can only be opened under their own will. The initiative for open data therefore shall focus on how to motivate private sectors releasing their own data-by ensuring profit and minimizing risks.

Originally, open data shall be available freely for everyone to use without any restrictions, and data owners may profit indirectly as users utilizing their data creating apps, etc. but not profit from open data itself. The income is unsteady and data owners therefore lose their interest to open data. As a countermeasure, it is suggested to make data chargeable though this may contradict to the definition of open data. When data owners can charge by usage or by time, the motivation of open data would arise when open data is directly profitable.

Data owners may also worry about many legal issues when releasing their own data. They may not care about whether profitable or not but afraid of being involved into litigation disputes such as intellectual property infringement, unfair competition, etc. It is very important for data owners to have a well protected authorization agreement when releasing data, but not all of them is able to afford the cost of making agreement for each data sharing. Therefore, a standard sample of contract that can be widely adopted plays a very important role for open private data.

A data sharing platform would be a solution to help data owners sharing their own data. It can not only provide a convenient way to collect profit from data sharing but help data owners avoiding legal risks with the platform’s standard agreement. All the data owners have to do is just to transfer their own data to the platform without concern since the platform would handle other affairs.

Ⅴ. Conclusion

Actively engaging the private sector in the open data value-chain is considered an innovation imperative as it is highly related to the development of information economy. Although many works still need to be done such as identifying mechanisms for catalyzing private sector engagement, these works can be done by organizations such as the World Bank and the Centre for Open Data Enterprise. Private-public collaboration is also important when it comes to strengthening the global data infrastructure, and the benefits of open data are diverse and range from improved efficiency of public administrations to economic growth in the private sector. However, open private data is not the goal but merely a start for open data revolution. It is to add variation for other organizations and individuals to analyze to create innovations while individuals, private sectors, or government will benefit from that innovation and being encouraged to release much more data to strengthen this data circulation.

[1] Global Open Data Index, https://index.okfn.org/place/(Last visited: May 15, 2017)

Reviews on Taiwan Constitutional Court's Judgment no. 13 of 2022 2022/11/24 I.Introduction In 2012, the Taiwan Human Rights Promotion Association and other civil groups believe that the National Health Insurance Administration released the national health insurance database and other health insurance data for scholars to do research without consent, which may be unconstitutional and petitioned for constitutional interpretation. Taiwan Human Rights Promotion Association believes that the state collects, processes, and utilizes personal data on a large scale with the "Personal Data Protection Law", but does not set up another law of conduct to control the exercise of state power, which has violated the principle of legal retention; the data is provided to third-party academic research for use, and the parties involved later Excessive restrictions on the right to withdraw go against the principle of proportionality. The claimant criticized that depriving citizens of their prior consent and post-control rights to medical data is like forcing all citizens to unconditionally contribute data for use outside the purpose before they can use health insurance. The personal data law was originally established to "avoid the infringement of personality rights and promote the rational use of data", but in the insufficient and outdated design of the regulations, it cannot protect the privacy of citizens' information from infringement, and it is easy to open the door to the use of data for other purposes. In addition, even if the health insurance data is de-identified, it is still "individual data" that can distinguish individuals, not "overall data." Health insurance data can be connected with other data of the Ministry of Health and Welfare, such as: physical and mental disability files, sexual assault notification files, etc., and you can also apply for bringing in external data or connecting with other agency data. Although Taiwan prohibits the export of original data, the risk of re-identification may also increase as the number of sources and types of data concatenated increases, as well as unspecified research purposes. The constitutional court of Taiwan has made its judgment on the constitutionality of the personal data usage of National Health Insurance research database. The judgment, released on August 12, 2022, states that Article 6 of Personal Data Protection Act(PDPA), which asks“data pertaining to a natural person's medical records, healthcare, genetics, sex life, physical examination and criminal records shall not be collected, processed or used unless where it is necessary for statistics gathering or academic research by a government agency or an academic institution for the purpose of healthcare, public health, or crime prevention, provided that such data, as processed by the data provider or as disclosed by the data collector, may not lead to the identification of a specific data subject”does not violate Intelligible principle and Principle of proportionality. Therefore, PDPA does not invade people’s right to privacy and remains constitutional. However, the judgment finds the absence of independent supervisory authority responsible for ensuring Taiwan institutions and bodies comply with data protection law, can be unconstitutional, putting personal data protection system on the borderline to failure. Accordingly, laws and regulations must be amended to protect people’s information privacy guaranteed by Article 22 of Constitution of the Republic of China (Taiwan). In addition, the judgment also states it is unconstitutional that Articles 79 and 80 of National Health Insurance Law and other relevant laws lack clear provisions in terms of store, process, external transmission of Personal health insurance data held by Central Health Insurance Administration of the Ministry of Health and Welfare. Finally, the Central Health Insurance Administration of the Ministry of Health and Welfare provides public agencies or academic research institutions with personal health insurance data for use outside the original purpose of collection. According to the overall observation of the relevant regulations, there is no relevant provision that the parties can request to “opt-out”; within this scope, it violates the intention of Article 22 of the Constitution to protect people's right to information privacy. II.Independent supervisory authority According to Article 3 of Central Regulations and Standards Act, government agencies can be divided into independent agencies that can independently exercise their powers and operate autonomously, and non- independent agencies that must obey orders from their superiors. In Taiwan, the so-called "dedicated agency"(專責機關) does not fall into any type of agency defined by the Central Regulations and Standards Act. Dedicated agency should be interpreted as an agency that is responsible for a specific business and here is no other agency to share the business. The European Union requires member states to set up independent regulatory agencies (refer to Articles 51 and 52 of General Data Protection Regulation (GDPR)). In General Data Protection Regulation and the adequacy reference guidelines, the specific requirements for personal data supervisory agencies are as follows: the country concerned should have one or more independent supervisory agencies; they should perform their duties completely independently and cannot seek or accept instructions; the supervisory agencies should have necessary and practicable powers, including the power of investigation; it should be considered whether its staff and budget can effectively assist its implementation. Therefore, in order to pass the EU's adequacy certification and implement the protection of people's privacy and information autonomy, major countries have set up independent supervisory agencies for personal data protection based on the GDPR standards. According to this research, most countries have 5 to 10 commissioners that independently exercise their powers to supervise data exchange and personal data protection. In order to implement the powers and avoid unnecessary conflicts of interests among personnel, most of the commissioners are full-time professionals. Article 3 of Basic Code Governing Central Administrative Agencies Organizations defines independent agency as "A commission-type collegial organization that exercises its powers and functions independently without the supervision of other agencies, and operates autonomously unless otherwise stipulated." It is similar to Japan, South Korea, and the United States. III.Right to Opt-out The judgment pointed out that the parties still have the right to control afterwards the personal information that is allowed to be collected, processed and used without the consent of the parties or that meets certain requirements. Although Article 11 of PDPA provides for certain parties to exercise the right to control afterwards, it does not cover all situations in which personal data is used, such as: legally collecting, processing or using correct personal data, and its specific purpose has not disappeared, In the event that the time limit has not yet expired, so the information autonomy of the party cannot be fully protected, the subject, cause, procedure, effect, etc. of the request for suspension of use should be clearly stipulated in the revised law, and exceptions are not allowed. The United Kingdom is of great reference. In 2017, after the British Information Commissioner's Office (ICO) determined that the data sharing agreement between Google's artificial intelligence DeepMind and the British National Health Service (NHS) violated the British data protection law, the British Department of Health and Social Care proposed National data opt-out Directive in May, 2018. British health and social care-related institutions may refer to the National Data Opt-out Operational Policy Guidance Document published by the National Health Service in October to plan the mechanism for exercising patient's opt-out right. The guidance document mainly explains the overall policy on the exercise of the right to opt-out, as well as the specific implementation of suggested practices, such as opt-out response measures, methods of exercising the opt-out right, etc. National Data Opt-out Operational Policy Guidance Document also includes exceptions and restrictions on the right to opt-out. The Document stipulates that exceptions may limit the right to Opt-out, including: the sharing of patient data, if it is based on the consent of the parties (consent), the prevention and control of infectious diseases (communicable disease and risks to public health), major public interests (overriding) Public interest), statutory obligations, or cooperation with judicial investigations (information required by law or court order), health and social care-related institutions may exceptionally restrict the exercise of the patient's right to withdraw. What needs to be distinguished from the situation in Taiwan is that when the UK first collected public information and entered it into the NHS database, there was already a law authorizing the NHS to search and use personal information of the public. The right to choose to enter or not for the first time; and after their personal data has entered the NHS database, the law gives the public the right to opt-out. Therefore, the UK has given the public two opportunities to choose through the enactment of special laws to protect public's right to information autonomy. At present, the secondary use of data in the health insurance database does not have a complete legal basis in Taiwan. At the beginning, the data was automatically sent in without asking for everyone’s consent, and there was no way to withdraw when it was used for other purposes, therefore it was s unconstitutional. Hence, in addition to thinking about what kind of provisions to add to the PDPA as a condition for "exception and non-request for cessation of use", whether to formulate a special law on secondary use is also worthy of consideration by the Taiwan government. IV.De-identification According to the relevant regulations of PDPA, there is no definition of "de-identification", resulting in a conceptual gap in the connotation. In other words, what angle or standard should be used to judge that the processed data has reached the point where it is impossible to identify a specific person. In judicial practice, it has been pointed out that for "data recipients", if the data has been de-identified, the data will no longer be regulated by PDPA due to the loss of personal attributes, and it is even further believed that de-identification is not necessary. However, the Judgment No. 13 of Constitutional Court, pointed out that through de-identification measures, ordinary people cannot identify a specific party without using additional information, which can be regarded as personal data of de-identification data. Therefore, the judge did not give an objective standard for de-identification, but believed that the purpose of data utilization and the risk of re-identification should be measured on a case-by-case basis, and a strict review of the constitutional principle of proportionality should be carried out. So far, it should be considered that the interpretation of the de-identification standard has been roughly finalized. V.Conclusions The judge first explained that if personal information is processed, the type and nature of the data can still be objectively restored to indirectly identify the parties, no matter how simple or difficult the restoration process is, if the data is restored in a specific way, the parties can still be identified. personal information. Therefore, the independent control rights of the parties to such data are still protected by Article 22 of the Constitution. Conversely, when the processed data objectively has no possibility to restore the identification of individuals, it loses the essence of personal data, and the parties concerned are no longer protected by Article 22 of the Constitution. Based on this, the judge declared that according to Article 6, Item 1, Proviso, Clause 4 of the PDPA, the health insurance database has been processed so that the specific party cannot be identified, and it is used by public agencies or academic research institutions for medical and health purposes. Doing necessary statistical or academic research complies with the principles of legal clarity and proportionality, and does not violate the Constitution. However, the judge believes that the current personal data law or other relevant regulations still lack an independent supervision mechanism for personal data protection, and the protection of personal information privacy is insufficient. In addition, important matters such as personal health insurance data can be stored, processed, and transmitted externally by the National Health Insurance Administration in a database; the subject, purpose, requirements, scope, and method of providing external use; and organizational and procedural supervision and protection mechanisms, etc. Articles 79 and 80 of the Health Insurance Law and other relevant laws lack clear provisions, so they are determined to be unconstitutional. In the end, the judge found that the relevant laws and regulations lacked the provisions that the parties can request to stop using the data, whether it is the right of the parties to request to stop, or the procedures to be followed to stop the use, there is no relevant clear text, obviously the protection of information privacy is insufficient. Therefore, regarding unconstitutional issues, the Constitutional Court ordered the relevant agencies to amend the Health Insurance Law and related laws within 3 years, or formulate specific laws.

Legal Opinion Led to Science and Technology Law: By the Mechanism of Policy Assessment of Industry and Social NeedsWith the coming of the Innovation-based economy era, technology research has become the tool of advancing competitive competence for enterprises and academic institutions. Each country not only has begun to develop and strengthen their competitiveness of industrial technology but also has started to establish related mechanism for important technology areas selected or legal analysis. By doing so, they hope to promote collaboration of university-industry research, completely bring out the economic benefits of the R & D. and select the right technology topics. To improve the depth of research cooperation and collect strategic advice, we have to use legislation system, but also social communication mechanism to explore the values and practical recommendations that need to be concerned in policy-making. This article in our research begins with establishing a mechanism for collecting diverse views on the subject, and shaping more efficient dialogue space. Finally, through the process of practicing, this study effectively collects important suggestions of practical experts.

The Research on ownership of cell therapy productsThe Research on ownership of cell therapy products 1. Issues concerning ownership of cell therapy products Regarding the issue of ownership interests, American Medical Association(AMA)has pointed out in 2016 that using human tissues to develop commercially available products raises question about who holds property rights in human biological materials[1]. In United States, there have been several disputes concern the issue of the whether the donor of the cell therapy can claim ownership of the product, including Moore v. Regents of University of California(1990)[2], Greenberg v. Miami Children's Hospital Research Institute(2003)[3], and Washington University v. Catalona(2007)[4]. The courts tend to hold that since cells and tissues were donated voluntarily, the donors had already lost their property rights of their cells and tissues at the time of the donation. In Moore case, even if the researchers used Moore’s cells to obtain commercial benefits in an involuntary situation, the court still held that the property rights of removed cells were not suitable to be claimed by their donor, so as to avoid the burden for researcher to clarify whether the use of cells violates the wishes of the donors and therefore decrease the legal risk for R&D activities. United Kingdom Medical Research Council(MRC)also noted in 2019 that the donated human material is usually described as ‘gifts’, and donors of samples are not usually regarded as having ownership or property rights in these[5]. Accordingly, both USA and UK tends to believe that it is not suitable for cell donors to claim ownership. 2. The ownership of cell therapy products in the lens of Taiwan’s Civil Code In Taiwan, Article 766 of Civil Code stipulated: “Unless otherwise provided by the Act, the component parts of a thing and the natural profits thereof, belong, even after their separation from the thing, to the owner of the thing.” Accordingly, many scholars believe that the ownership of separated body parts of the human body belong to the person whom the parts were separated from. Therefore, it should be considered that the ownership of the cells obtained from the donor still belongs to the donor. In addition, since it is stipulated in Article 406 of Civil Code that “A gift is a contract whereby the parties agree that one of the parties delivers his property gratuitously to another party and the latter agrees to accept it.”, if the act of donation can be considered as a gift relationship, then the ownership of the cells has been delivered from donor to other party who accept it accordingly. However, in the different versions of Regenerative Medicine Biologics Regulation (draft) proposed by Taiwan legislators, some of which replace the term “donor” with “provider”. Therefore, for cell providers, instead of cell donors, after providing cells, whether they can claim ownership of cell therapy product still needs further discussion. According to Article 69 of the Civil Code, it is stipulated that “Natural profits are products of the earth, animals, and other products which are produced from another thing without diminution of its substance.” In addition, Article 766 of the Civil Code stipulated that “Unless otherwise provided by the Act, the component parts of a thing and the natural profits thereof, belong, even after their separation from the thing, to the owner of the thing.” Thus, many scholars believe that when the product is organic, original substance and the natural profits thereof are all belong to the owner of the original substance. For example, when proteins are produced from isolated cells, the proteins can be deemed as natural profits and the ownership of proteins and isolated cells all belong to the owner of the cells[6]. Nevertheless, according to Article 814 of the Civil Code, it is stipulated that “When a person has contributed work to a personal property belonging to another, the ownership of the personal property upon which the work is done belongs to the owner of the material thereof. However, if the value of the contributing work obviously exceeds the value of the material, the ownership of the personal property upon which the work is done belongs to the contributing person.” Thus, scholar believes that since regenerative medical technology, which induces cell differentiation, involves quite complex biotechnology technology, and should be deemed as contributing work. Therefore, the ownership of cell products after contributing work should belongs to the contributing person[7]. Thus, if the provider provides the cells to the researcher, after complex biotechnology contributing work, the original ownership of the cells should be deemed to have been eliminated, and there is no basis for providers to claim ownership. However, since the development of cell therapy products involves a series of R&D activities, it still need to be clarified that who is entitled to the ownership of the final cell therapy products. According to Taiwan’s Civil Code, the ownership of product after contributing work should belongs to the contributing person. However, when there are numerous contributing persons, which person should the ownership belong to, might be determined on a case-by-case basis. 3. Conclusion The biggest difference between cell therapy products and all other small molecule drugs or biologics is that original cell materials are provided by donors or providers, and the whole development process involves numerous contributing persons. Hence, ownership disputes are prone to arise. In addition to the above-discussed disputes, United Kingdom Co-ordinating Committee on Cancer Research(UKCCCR)also noted that there is a long list of people and organizations who might lay claim to the ownership of specimens and their derivatives, including the donor and relatives, the surgeon and pathologist, the hospital authority where the sample was taken, the scientists engaged in the research, the institution where the research work was carried out, the funding organization supporting the research and any collaborating commercial company. Thus, the ultimate control of subsequent ownership and patent rights will need to be negotiated[8]. Since the same issues might also occur in Taiwan, while developing cell therapy products, carefully clarifying the ownership between stakeholders is necessary for avoiding possible dispute. [1]American Medical Association [AMA], Commercial Use of Human Biological Materials, Code of Medical Ethics Opinion 7.3.9, Nov. 14, 2016, https://www.ama-assn.org/delivering-care/ethics/commercial-use-human-biological-materials (last visited Jan. 3, 2021). [2]Moore v. Regents of University of California, 793 P.2d 479 (Cal. 1990) [3]Greenberg v. Miami Children's Hospital Research Institute, 264 F. Suppl. 2d, 1064 (SD Fl. 2003) [4]Washington University v. Catalona, 490 F 3d 667 (8th Cir. 2007) [5]Medical Research Council [MRC], Human Tissue and Biological Samples for Use in Research: Operational and Ethical Guidelines, 2019, https://mrc.ukri.org/publications/browse/human-tissue-and-biological-samples-for-use-in-research/ (last visited Jan. 3, 2021). [6]Wen-Hui Chiu, The legal entitlement of human body, tissue and derivatives in civil law, Angle Publishing, 2016, at 327. [7]id, at 341. [8]Okano, M., Takebayashi, S., Okumura, K., Li, E., Gaudray, P., Carle, G. F., & Bliek, J. UKCCCR guidelines for the use of cell lines in cancer research.Cytogenetic and Genome Research,86(3-4), 1999, https://europepmc.org/backend/ptpmcrender.fcgi?accid=PMC2363383&blobtype=pdf (last visited Jan. 3, 2021).

Taiwan Planed Major Promoting Program for Biotechnology and Pharmaceutical IndustryTaiwan Government Lauched the “Biotechnology Action Plan” The Taiwan Government has planned to boost the support and develop local industries across the following six major sectors: biotechnology, tourism, health care, green energy, innovative culture and post-modern agriculture. As the biotechnology industry has reached its maturity by the promulgation of "Biotech and New Pharmaceutical Development Act" in July, 2007, it will be the first to take the lead among the above sectors. Thus, the Executive Yuan has launched the Biotechnology Action Plan as the first project in building the leading industry sectors, to upgrade local industries and stimulate future economic growth. Taiwan Government Planed to Promote the Biotechnology and Other newly Industries by Investing Two Hundred Billion To expand every industrial scale, enhance industrial value, increase the value around the main industrial field, and to encourage the industrial development by government investments for creating the civil working opportunities to reach the goal of continuous economic development, the Executive Yuan Economic Establishment commission has expressed that, the government has selected six newly industrials including "Biotechnology", "Green Energy", "Refined Agriculture", "Tourism", "Medicare", and "Culture Originality" on November 19, 2009 to promote our national economic growth. The government will invest two hundred billion NT dollars to support the industrial development aggressively and to enhance the social investments from year 2009 to 2012. According to a Chung-Hua Institution for Economic Research report, the future growth rate will reach 8.16% after the evaluation, Hence, the future of the industries seems to be quite bright. Currently, the government plans to put money into six newly industries through the existing ways for investment. For instance, firstly, in accordance with the "Act For The Development Of Biotech And New Pharmaceuticals Industry" article 5 provision 1 ",for the purpose of promoting the Biotech and New Pharmaceuticals Industry, a Biotech and New Pharmaceuticals Company may, for a period of five years from the time it is subject to corporate income tax, enjoy a reduction in its corporate income tax payable for up to thirty-five percent (35%) of the total funds invested in research and development ("R&D") and personnel training each year; provided, however, that if the R&D expenditure of a particular year exceeds the average R&D expenditure of the previous two years or if the personnel training expenditure of a particular year exceeds the average personnel training expenditure of the previous two years, fifty percent (50%) of the amount in excess of the average may be used to credit against the amount of corporate income tax payable. Secondly, according to same act of the article 6 provision 1 ", in order to encourage the establishment or expansion of Bio tech and New Pharmaceuticals Companies, a profit-seeking enterprise that (i) subscribes for the stock issued by a Biotech and New Pharmaceuticals Company at the time of the latter's establishment or subsequent expansion; and (ii) has been a registered shareholder of the Biotech and New Pharmaceuticals Company for a period of three (3) years or more, may, for a period of five years from the time it is subject to corporate income tax, enjoy a reduction in its corporate income tax payable for up to twenty percent (20%) of the total amount of price paid for the subscription of shares in such Biotech and New Pharmaceuticals Company; provided that such Biotech and New Pharmaceuticals Company has not applied for exemption from corporate income tax or shareholders investment credit based on the subscription price under other applicable laws and regulations. Thirdly, to promote the entire biotechnological industry development, the government has drafted the "Biotechnology Takeoff Package" for subsidizing the startup´s social investment companies which can satisfy the conditions to invest in "Drug discovery", "Medical Device" or other related biotech industries up to 5 billion with the capital invest in domestic industry over 50%, , with operating experience of multinational biotech investment companies with capital over 150 million in related industrial fields, and with the working experiences of doctor accumulated up to 60 years. Additionally, the refined agriculture industry field has not only discovered the gene selected products, but also combined the tourism with farming business for new business model creation. According to the "Guidelines for Preferential Loans for the Upgrading of Tourism Enterprises" point 4 provision 1, the expenditure for spending on machine, instruments, land or repairing can be granted a preferential loan in accordance with the rule of point 6, and government will provide a subsidy of interest for loaning Tourism Enterprises with timely payments. At last, Council for Economic Planning and Development also points out because most of technology industry has been impacted seriously by fluctuation of international prosperity due to conducting the export trade oriented strategy. Furthermore, the aspects of our export trade of technology industry have been impacted by the U.S. financial crisis and the economic decay in EU and US; and the industrial development seems to face the problem caused by over centralization in Taiwan. Hence, the current framework of domestic industry should be rearranged and to make it better by promoting the developmental project of six newly industries. Taiwan Government Had Modifies Rules to Accelerate NDA Process and Facilitate Development of Clinical Studies in Taiwan In July 2007, the "Biotech and New Pharmaceutical Development Act" modified many regulations related to pharmaceutical administration, taxes, and professionals in Taiwan. In addition, in order to facilitate the development of the biotechnology and pharmaceutical industries, the government has attempted to create a friendly environment for research and development by setting up appropriate regulations and application systems. These measures show that the Taiwanese government is keenly aware that these industries have huge potential value. To operate in coordination with the above Act and to better deal with the increasing productivity of pharmaceutical R&D programs in Taiwan, the Executive Yuan simplified the New Drug Application (NDA) process to facilitate the submission that required Certificate of Pharmaceutical Product (CPP) for drugs with new ingredients. The current NDA process requires sponsors to submit documentation as specified by one of the following four options: (1) three CPPs from three of "ten medically-advanced countries," including Germany, the U.S., England, France, Japan, Switzerland, Canada, Australia, Belgium, and Sweden; (2) one CPP from the U.S., Japan, Canada, Australia, or England and one CPP from Germany, France, Switzerland, Sweden, or Belgium; (3) a Free Sale Certificate (FSC) from one of ten medically-advanced countries where the pharmaceuticals are originally produced and one CPP from one of the other nine countries; or (4) a CPP from the European Medicines Agency. Thus, the current NDA process requires sponsors to spend inordinate amounts of time and incur significant costs to acquire two or three FSCs or CPPs from ten medically-advanced countries in order to submit an NDA in Taiwan. According to the new rules, sponsors will not have to submit above CPPs if (1) Phase I clinical studies have been conducted in Taiwan, and Phase III Pivotal Trial clinical studies have been simultaneously conducted both in Taiwan and in another country or (2) Phase II and Phase III Pivotal Trial clinical studies have been simultaneously conducted both in Taiwan and in another country. Besides, the required minimum numbers of patients were evaluated during each above phase. Therefore, sponsors who conduct clinical studies in Taiwan and in another country simultaneously could reduce their costs and shorten the NDA process in Taiwan. The new rules aim to encourage international pharmaceutical companies to conduct clinical studies in Taiwan or to conduct such studies cooperatively with Taiwanese pharmaceutical companies. Such interactions will allow Taiwanese pharmaceutical companies to participate in development and implementation of international clinical studies in addition to benefiting from the shortened NDA process. Therefore, the R&D abilities and the internationalization of the Taiwanese pharmaceutical industry will be improved.

- Impact of Government Organizational Reform to Scientific Research Legal System and Response Thereto (1) – For Example, The Finnish Innovation Fund (“SITRA”)

- The Demand of Intellectual Property Management for Taiwanese Enterprises

- Blockchain in Intellectual Property Protection

- Impact of Government Organizational Reform to Research Legal System and Response Thereto (2) – Observation of the Swiss Research Innovation System

- Recent Federal Decisions and Emerging Trends in U.S. Defend Trade Secrets Act Litigation

- The effective and innovative way to use the spectrum: focus on the development of the "interleaved/white space"

- Copyright Ownership for Outputs by Artificial Intelligence

- Impact of Government Organizational Reform to Research Legal System and Response Thereto (2) – Observation of the Swiss Research Innovation System