Impact of Government Organizational Reform to Scientific Research Legal System and Response Thereto (1) – For Example, The Finnish Innovation Fund (“SITRA”)

Impact of Government Organizational Reform to Scientific Research Legal System and Response Thereto (1) – For Example, The Finnish Innovation Fund (“SITRA”)

I. Foreword

We hereby aim to analyze and research the role played by The Finnish Innovation Fund (“Sitra”) in boosting the national innovation ability and propose the characteristics of its organization and operation which may afford to facilitate the deliberation on Taiwan’s legal system. Sitra is an independent organization which is used to reporting to the Finnish Parliament directly, dedicated to funding activities to boost sustainable development as its ultimate goal and oriented toward the needs for social change. As of 2004, it promoted the fixed-term program. Until 2012, it, in turn, primarily engaged in 3-year program for ecological sustainable development and enhancement of society in 2012. The former aimed at the sustainable use of natural resources to develop new structures and business models and to boost the development of a bioeconomy and low-carbon society, while the latter aimed to create a more well-being-oriented public administrative environment to upgrade various public sectors’ leadership and decision-making ability to introduce nationals’ opinion to policies and the potential of building new business models and venture capital businesses[1].

II. Standing and Operating Instrument of Sitra

1. Sitra Standing in Boosting of Finnish Innovation Policies

(1) Positive Impact from Support of Innovation R&D Activities by Public Sector

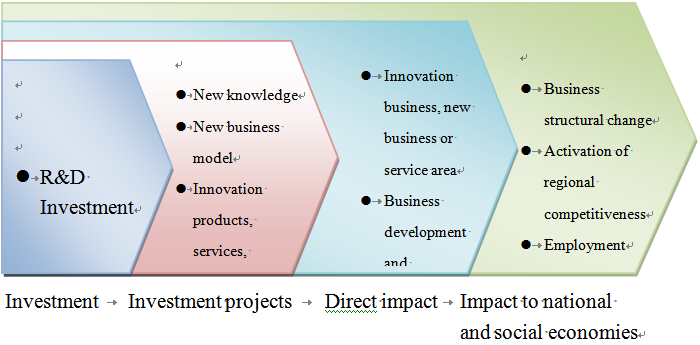

Utilization of public sector’s resources to facilitate and boost industrial innovation R&D ability is commonly applied in various countries in the world. Notwithstanding, the impact of the public sector’s investment of resources produced to the technical R&D and the entire society remains explorable[2]. Most studies still indicate positive impact, primarily as a result of the market failure. Some studies indicate that the impact of the public sector’s investment of resources may be observable at least from several points of view, including: 1. The direct output of the investment per se and the corresponding R&D investment potentially derived from investees; 2. R&D of outputs derived from the R&D investment, e.g., products, services and production methods, etc.; 3. direct impact derived from the R&D scope, e.g., development of a new business, or new business and service models, etc.; 4. impact to national and social economies, e.g., change of industrial structures and improvement of employment environment, etc. Most studies indicate that from the various points of view, the investment by public sector all produced positive impacts and, therefore, such investment is needed definitely[3]. The public sector may invest in R&D in diversified manners. Sitra invests in the “market” as an investor of corporate venture investment market, which plays a role different from the Finnish Funding Agency for Technology and Innovation (“Tekes”), which is more like a governmental subsidizer. Nevertheless, Finland’s characteristics reside in the combination of multiple funding and promotion models. Above all, due to the different behavior model, the role played by the former is also held different from those played by the general public sectors. This is why we choose the former as the subject to be studied herein.

Data source: Jari Hyvärinen & Anna-Maija Rautiainen, Measuring additionality and systemic impacts of public research and development funding – the case of TEKES, FINLAND, RESEARCH EVALUATION, 16(3), 205, 206 (2007).

Fig. 1 Phased Efforts of Resources Invested in R&D by Public Sector

(2) Two Sided f Role Played by Sitra in Boosting of Finnish Innovation Policies

Sitra has a very special position in Finland’s national innovation policies, as it not only helps successful implementation of the innovation policies but also acts an intermediary among the relevant entities. Sitra was founded in 1967 under supervision of the Bank of Finland before 1991, but was transformed into an independent foundation under the direction of the Finnish Parliament[4].

Though Sitra is a public foundation, its operation will not be intervened or restricted by the government. Sitra may initiate any innovation activities for its new organization or system, playing a role dedicated to funding technical R&D or promoting venture capital business. Meanwhile, Sitra also assumes some special function dedicated to decision-makers’ training and organizing decision-maker network to boost structural change. Therefore, Sitra may be identified as a special organization which may act flexibly and possess resources at the same time and, therefore, may initiate various innovation activities rapidly[5].

Sitra is authorized to boost the development of innovation activities in said flexible and characteristic manner in accordance with the Finland Innovation Fund Act (Laki Suomen itsenäisyyden juhlarahastosta). According to the Act, Finland established Sitra in 1967 and Sitra was under supervision of Bank of Finland (Article 1). Sitra was established in order to boost the stable growth of Finland’s economy via the national instrument’s support of R&D and education or other development instruments (Article 2). The policies which Sitra may adopt include loaning or funding, guarantee, marketable securities, participation in cooperative programs, partnership or equity investment (Article 3). If necessary, Sitra may collect the title of real estate or corporate shares (Article 7).

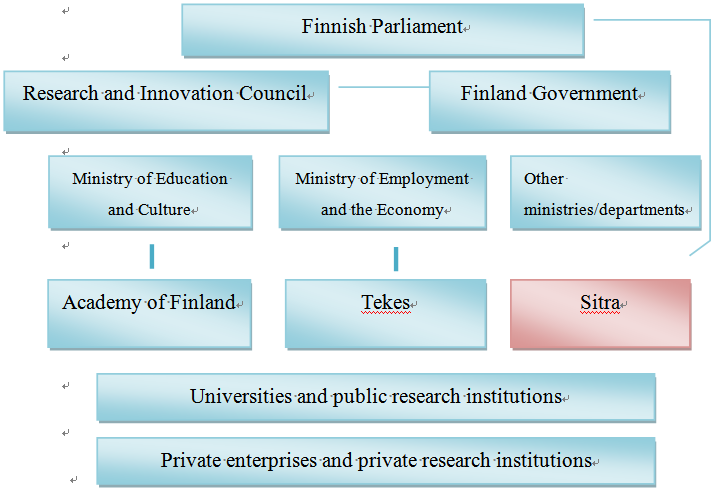

Data source: Finnish innovation system, Research.fi, http://www.research.fi/en/innovationsystem.html (last visited Mar. 15, 2013).

Fig. 2 Finnish Scientific Research Organization Chart

Sitra's innovation role has been evolved through two changes. Specifically, Sitra was primarily dedicated to funding technical R&D among the public sectors in Finland, and the funding model applied by Sitra prior to the changes initiated the technical R&D promotion by Tekes, which was established in 1983. The first change of Sitra took place in 1987. After that, Sitra turned to focus on the business development and venture capital invested in technology business and led the venture capital investment. Meanwhile, it became a partner of private investment funds and thereby boosted the growth of venture capital investments in Finland in 1990. In 2000, the second change of Sitra took place and Sitra’s organization orientation was changed again. It achieved the new goal for structural change step by step by boosting the experimental social innovation activities. Sitra believed that it should play the role contributing to procedural change and reducing systematic obstacles, e.g., various organizational or institutional deadlocks[6].

Among the innovation policies boosted by the Finnish Government, the support of Start-Ups via governmental power has always been the most important one. Therefore, the Finnish Government is used to playing a positive role in the process of developing the venture capital investment market. In 1967, the Government established a venture capital company named Sponsor Oy with the support from Bank of Finland, and Sponsor Oy was privatized after 1983. Finland Government also established Kera Innovation Fund (now known as Finnvera[7]) in 1971, which was dedicated to boosting the booming of Start-Ups in Finland jointly with Finnish Industry Investment Ltd. (“FII”) established by the Government in 1994, and Sitra, so as to make the “innovation” become the main development force of the country[8] .

Sitra plays a very important role in the foundation and development of venture capital market in Finland and is critical to the Finnish Venture Capital Association established in 1990. After Bank of Finland was under supervision of Finnish Parliament in 1991, Sitra became on the most important venture capital investors. Now, a large portion of private venture capital funds are provided by Sitra[9]. Since Sitra launched the new strategic program in 2004, it has turned to apply smaller sized strategic programs when investing young innovation companies, some of which involved venture capital investment. The mapping of young innovation entrepreneurs and angel investors started as of 1996[10].

In addition to being an important innovation R&D promoter in Finland, Sitra is also an excellent organization which is financially self-sufficient and tends to gain profit no less than that to be generated by a private enterprise. As an organization subordinated to the Finnish Parliament immediately, all of Sitra’s decisions are directly reported to the Parliament (public opinion). Chairman of Board, Board of Directors and supervisors of Sitra are all appointed by the Parliament directly[11]. Its working funds are generated from interest accruing from the Fund and investment income from the Fund, not tax revenue or budget prepared by the Government any longer. The total fund initially founded by Bank of Finland amounted to DEM100,000,000 (approximately EUR17,000,000), and was accumulated to DEM500,000,000 (approximately EUR84,000,000) from 1972 to 1992. After that, following the increase in market value, its nominal capital amounted to DEM1,400,000,000 (approximately EUR235,000,000) from 1993 to 2001. Obviously, Sitra generated high investment income. Until 2010, it has generated the investment income amounting to EUR697,000,000 .

In fact, Sitra’s concern about venture capital investment is identified as one of the important changes in Finland's national technical R&D polices after 1990[13]. Sitra is used to funding businesses in three manners, i.e., direct investment in domestic stock, investment in Finnish venture capital funds, and investment in international venture capital funds, primarily in four industries, technology, life science, regional cooperation and small-sized & medium-sized starts-up. Meanwhile, it also invests in venture capital funds for high-tech industries actively. In addition to innovation technology companies, technical service providers are also its invested subjects[14].

2. “Investment” Instrument Applied by Sitra to Boost Innovation Business

The Starts-Up funding activity conducted by Sitra is named PreSeed Program, including INTRO investors’ mapping platform dedicated to mapping 450 angel investment funds and entrepreneurs, LIKSA engaged in working with Tekes to funding new companies no more than EUR40,000 for purchase of consultation services (a half thereof funded by Tekes, and the other half funded by Sitra in the form of loan convertible to shares), DIILI service[15] dedicated to providing entrepreneurs with professional sale consultation resources to integrate the innovation activity (product thereof) and the market to remedy the deficit in the new company’s ability to sell[16].

The investment subjects are stated as following. Sitra has three investment subjects, namely, corporate investments, fund investments and project funding.

(1) Corporate investment

Sitra will not “fund” enterprises directly or provide the enterprises with services without consideration (small-sized and medium-sized enterprises are aided by other competent authorities), but invest in the businesses which are held able to develop positive effects to the society, e.g., health promotion, social problem solutions, utilization of energy and effective utilization of natural resources. Notwithstanding, in order to seek fair rate of return, Sitra is dedicated to making the investment (in various enterprises) by its professional management and technology, products or competitiveness of services, and ranging from EUR300,000 to EUR1,000,000 to acquire 10-30% of the ownership of the enterprises, namely equity investment or convertible funding. Sitra requires its investees to value corporate social responsibility and actively participate in social activities. It usually holds the shares from 4 years to 10 years, during which period it will participate the corporate operation actively (e.g., appointment of directors)[17].

(2) Fund investments

For fund investments[18], Sitra invests in more than 50 venture capital funds[19]. It invests in domestic venture capital fund market to promote the development of the market and help starts-up seek funding and create new business models, such as public-private partnerships. It invests in international venture capital funds to enhance the networking and solicit international funding, which may help Finnish enterprises access international trend information and adapt to the international market.

(3) Project funding

For project funding, Sitra provides the on-site information survey (supply of information and view critical to the program), analysis of business activities (analysis of future challenges and opportunities) and research & drafting of strategies (collection and integration of professional information and talents to help decision making), and commissioning of the program (to test new operating model by commissioning to deal with the challenge from social changes). Notwithstanding, please note that Sitra does not invest in academic study programs, research papers or business R&D programs[20].

(4) DIILI Investment Model Integrated With Investment Absorption

A Start-Up usually will not lack technologies (usually, it starts business by virtue of some advanced technology) or foresighted philosophy when it is founded initially, while it often lacks the key to success, the marketing ability. Sitra DIILI is dedicated to providing the professional international marketing service to help starts-up gain profit successfully. Owing to the fact that starts-up are usually founded by R&D personnel or research-oriented technicians, who are not specialized in marketing and usually retains no sufficient fund to employ marketing professionals, DILLI is engaged in providing dedicated marketing talents. Now, it employs about 85 marketing professionals and seeks to become a start-up partner by investing technical services.

Notwithstanding, in light of the characteristics of Sitra’s operation and profitability, some people indicate that it is more similar to a developer of an innovation system, rather than a neutral operator. Therefore, it is not unlikely to hinder some work development which might be less profitable (e.g., establishment of platform). Further, Sitra is used to developing some new investment projects or areas and then founding spin-off companies after developing the projects successfully. The way in which it operates seems to be non-compatible with the development of some industries which require permanent support from the public sector. The other issues, such as INTRO lacking transparency and Sitra's control over investment objectives likely to result in adverse choice, all arise from Sitra’s consideration to its own investment opportunities and profit at the same time of mapping. Therefore, some people consider that it should be necessary to move forward toward a more transparent structure or a non-income-oriented funding structure[21] . Given this, the influence of Sitra’s own income over upgrading of the national innovation ability when Sitra boosts starts-up to engage in innovation activities is always a concern remaining disputable in the Finnish innovation system.

3. Boosting of Balance in Regional Development and R&D Activities

In order to fulfill the objectives under Lisbon Treaty and to enable EU to become the most competitive region in the world, European Commission claims technical R&D as one of its main policies. Among other things, under the circumstance that the entire R&D competitiveness upgrading policy is always progressing sluggishly, Finland, a country with a population of 5,300,000, accounting for 1.1% of the population of 27 EU member states, was identified as the country with the No. 1 innovation R&D ability in the world by World Economic Forum in 2005. Therefore, the way in which it promotes innovation R&D policies catches the public eyes. Some studies also found that the close relationship between R&D and regional development policies of Finland resulted in the integration of regional policies and innovation policies, which were separated from each other initially, after 1990[22]. Finland has clearly defined the plan to exploit the domestic natural resources and human resources in a balanced and effective manner after World War II. At the very beginning, it expanded the balance of human resources to low-developed regions, in consideration of the geographical politics, but in turn, it achieved national balanced development by meeting the needs for a welfare society and mitigation of the rural-urban divide as time went by. The Finnish innovation policies which may resort to technical policies retroactively initially drove the R&D in the manners including upgrading of education degree, founding of Science and Technology Policy Council and Sitra, establishment of Academy of Finland (1970) and establishment of the technical policy scheme, et al.. Among other things, people saw the role played by Sitra in Finland’s knowledge-intensive society policy again. From 1991 to 1995, the Finnish Government officially included the regional competitiveness into the important policies. The National Industrial Policy for Finland in 1993 adopted the strategy focusing on the development based on competitive strength in the regional industrial communities[23].

Also, some studies indicated that in consideration of Finland’s poor financial and natural resources, its national innovation system should concentrate the resources on the R&D objectives which meet the requirements about scale and essence. Therefore, the “Social Innovation, Social and Economic Energy Re-building Learning Society” program boosted by Sitra as the primary promoter in 2002 defined the social innovation as “the reform and action plan to enhance the regulations of social functions (law and administration), politics and organizational structure”, namely reform of the mentality and cultural ability via social structural changes that results in social economic changes ultimately. Notwithstanding, the productivity innovation activity still relies on the interaction between the enterprises and society. Irrelevant with the Finnish Government’s powerful direction in technical R&D activities, in fact, more than two-thirds (69.1%) of the R&D investment was launched by private enterprises and even one-thirds launched by a single enterprise (i.e., Nokia) in Finland. At the very beginning of 2000, due to the impact of globalization to Finland’s innovation and regional policies, a lot of R&D activities were emigrated to the territories outside Finland[24]. Multiple disadvantageous factors initiated the launch of national resources to R&D again. The most successful example about the integration of regional and innovation policies in Finland is the Centres of Expertise Programme (CEP) boosted by it as of 1990. Until 1994, there have been 22 centres of expertise distributed throughout Finland. The centres were dedicated to integrating local universities, research institutions and enterprise for co-growth. The program to be implemented from 2007 to 2013 planned 21 centres of expertise (13 groups), aiming to promote the corporate sectors’ cooperation and innovation activities. CEP integrated local, regional and national resources and then focused on the businesses designated to be developed[25].

[1] Sitra, http://www.sitra.fi/en (last visited Mar. 10, 2013).

[2] Jari Hyvärinen & Anna-Maija Rautiainen, Measuring additionality and systemic impacts of public research and development funding – the case of TEKES, FINLAND, RESEARCH EVALUATION, 16(3), 205, 208 (2007).

[3] id. at 206-214.

[4] Charles Edquist, Tterttu Luukkonen & Markku Sotarauta, Broad-Based Innovation Policy, in EVALUATION OF THE FINNISH NATIONAL INNOVATION SYSTEM – FULL REPORT 11, 25 (Reinhilde Veugelers st al. eds., 2009).

[5] id.

[6] id.

[7] Finnvera is a company specialized in funding Start-Ups, and its business lines include loaning, guarantee, venture capital investment and export credit guarantee, etc. It is a state-run enterprise and Export Credit Agency (ECA) in Finland. Finnvera, http://annualreport2012.finnvera.fi/en/about-finnvera/finnvera-in-brief/ (last visited Mar. 10, 2013).

[8] Markku Maula, Gordon Murray & Mikko Jääskeläinen, MINISTRY OF TRADE AND INDUSTRY, Public Financing of Young Innovation Companies in Finland 32 (2006).

[9] id. at 33.

[10] id. at 41.

[11] Sitra, http://www.sitra.fi/en (last visited Mar. 10, 2013).

[12] Sitra, http://www.sitra.fi/en (last visited Mar. 10, 2013).

[13] The other two were engaged in boosting the regional R&D center and industrial-academy cooperative center programs. Please see Gabriela von Blankenfeld-Enkvist, Malin Brännback, Riitta Söderlund & Marin Petrov, ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT [OECD],OECD Case Study on Innovation: The Finnish Biotechnology Innovation System 15 (2004).

[14] id. at20.

[15] DIILI service provides sales expertise for SMEs, Sitra, http://www.sitra.fi/en/articles/2005/diili-service-provides-sales-expertise-smes-0 (last visited Mar. 10, 2013).

[16] Maula, Murray & Jääskeläinen, supra note 8 at 41-42.

[17] Corporate investments, Sitra, http://www.sitra.fi/en/corporate-investments (last visited Mar. 10, 2013).

[18] Fund investments, Sitra, http://www.sitra.fi/en/fund-investments (last visited Mar. 10, 2013).

[19] The venture capital funds referred to herein mean the pooled investment made by the owners of venture capital, while whether it exists in the form of fund or others is not discussed herein.

[20] Project funding, Sitra, http://www.sitra.fi/en/project-funding (last visited Mar. 10, 2013).

[21] Maula, Murray & Jääskeläinen, supra note 8 at 42.

[22] Jussi S. Jauhiainen, Regional and Innovation Policies in Finland – Towards Convergence and/or Mismatch? REGIONAL STUDIES, 42(7), 1031, 1032-1033 (2008).

[23] id. at 1036.

[24] id. at 1038.

[25] id. at 1038-1039.

Blockchain and General Data Protection Regulation (GDPR) compliance issues (2019) I. Brief Blockchain technology can solve the problem of trust between data demanders and data providers. In other words, in a centralized mode, data demanders can only choose to believe that the centralized platform will not contain the false information. However, in the decentralized mode, data isn’t controlled by one individual group or organization[1], data demanders can directly verify information such as data source, time, and authorization on the blockchain without worrying about the correctness and authenticity of the data. Take the “immutable” for example, it is conflict with the right to erase (also known as the right to be forgotten) in the GDPR.With encryption and one-time pad (OTP) technology, data subjects can make data off-chain storaged or modified at any time in a decentralized platform, so the problem that data on blockchain not meet the GDPR regulation has gradually faded away. II. What is GDPR? The purpose of the EU GDPR is to protect user’s data and to prevent large-scale online platforms or large enterprises from collecting or using user’s data without their permission. Violators will be punished by the EU with up to 20 million Euros (equal to 700 million NT dollars) or 4% of the worldwide annual revenue of the prior financial year. The aim is to promote free movement of personal data within the European Union, while maintaining adequate level of data protection. It is a technology-neutral law, any type of technology which is for processing personal data is applicable. So problem about whether the data on blockchain fits GDPR regulation has raise. Since the blockchain is decentralized, one of the original design goals is to avoid a large amount of centralized data being abused. Blockchain can be divided into permissioned blockchains and permissionless blockchains. The former can also be called “private chains” or “alliance chains” or “enterprise chains”, that means no one can join the blockchain without consent. The latter can also be called “public chains”, which means that anyone can participate on chain without obtaining consent. Sometimes, private chain is not completely decentralized. The demand for the use of blockchain has developed a hybrid of two types of blockchain, called “alliance chain”, which not only maintains the privacy of the private chain, but also maintains the characteristics of public chains. The information on the alliance chain will be open and transparent, and it is in conflict with the application of GDPR. III. How to GDPR apply to blockchain ? First, it should be determined whether the data on the blockchain is personal data protected by GDPR. Second, what is the relationship and respective responsibilities of the data subject, data controller, and data processor? Finally, we discuss the common technical characteristics of blockchain and how it is applicable to GDPR. 1. Data on the blockchain is personal data protected by GDPR? First of all, starting from the technical characteristics of the blockchain, blockchain technology is commonly decentralized, anonymous, immutable, trackable and encrypted. The other five major characteristics are immutability, authenticity, transparency, uniqueness, and collective consensus. Further, the blockchain is an open, decentralized ledger technology that can effectively verify and permanently store transactions between two parties, and can be proved. It is a distributed database, all users on the chain can access to the database and the history record, also can directly verify transaction records. Each nodes use peer-to-peer transmission for upload or transfer information without third-party intermediation, which is the unique “decentralization” feature of the blockchain. In addition, the node or any user on the chain has a unique and identifiable set of more than 30 alphanumeric addresses, but the user may choose to be anonymous or provide identification, which is also a feature of transparency with pseudonymity[2]; Data on blockchain is irreversibility of records. Once the transaction is recorded and updated on the chain, it is difficult to change and is permanently stored in the database, that is to say, it has the characteristics of “tamper-resistance”[3]. According to Article 4 (1) of the GDPR, “personal data” means any information relating to an identified or identifiable natural person (‘data subject’); an identifiable natural person is one who can be identified, directly or indirectly, in particular by reference to an identifier such as a name, an identification number, location data, an online identifier or to one or more factors specific to the physical, physiological, genetic, mental, economic, cultural or social identity of that natural person. Therefore, if data subject cannot be identified by the personal data on the blockchain, that is an anonymous data, excluding the application of GDPR. (1) What is Anonymization? According to Opinion 05/2014 on Anonymization Techniques by Article 29 Data Protection Working Party of the European Union, “anonymization” is a technique applied to personal data in order to achieve irreversible de-identification[4]. And it also said the “Hash function” of blockchain is a pseudonymization technology, the personal data is possible to be re-identified. Therefore it’s not an “anonymization”, the data on the blockchain may still be the personal data stipulated by the GDPR. As the blockchain evolves, it will be possible to develop technologies that are not regulated by GDPR, such as part of the encryption process, which will be able to pass the court or European data protection authorities requirement of anonymization. There are also many compliance solutions which use technical in the industry, such as avoiding transaction data stored directly on the chain. 2. International data transmission Furthermore, in accordance with Article 3 of the GDPR, “This Regulation applies to the processing of personal data in the context of the activities of an establishment of a controller or a processor in the Union, regardless of whether the processing takes place in the Union or not. This Regulation applies to the processing of personal data of data subjects who are in the Union by a controller or processor not established in the Union, where the processing activities are related to: (a) the offering of goods or services, irrespective of whether a payment of the data subject is required, to such data subjects in the Union; or (b) the monitoring of their behaviour as far as their behaviour takes place within the Union”.[5] In other words, GDPR applies only when the data on the blockchain is not anonymized, and involves the processing of personal data of EU citizens. 3. Identification of data controllers and data processors Therefore, if the encryption technology involves the public storage of EU citizens' personal data and passes it to a third-party controller, it may be identified as the “data controller” under Article 4 of GDPR, and all nodes and miners of the platform may be deemed as the “co-controller” of the data, and be assumed joint responsibility with the data controller by GDPR. For example, the parties can claim the right to delete data from the data controller. In addition, a blockchain operator may be identified as a “processor”, for example, Backend as a Service (BaaS) products, the third parties provide network infrastructure for users, and let users manage and store personal data. Such Cloud Services Companies provide online services on behalf of customers, do not act as “data controllers”. Some commentators believe that in the case of private chains or alliance chains, such as land records transmission, inter-bank customer information sharing, etc., compared to public chain applications: such as cryptocurrencies (Bitcoin for example), is not completely decentralized, and more likely to meet GDPR requirements[6]. For example, in the case of a private chain or alliance chain, it is a closed platform, which contains only a small number of trusted nodes, is more effective in complying with the GDPR rules. 4. Data subject claims In accordance with Article 17 of the GDPR, The data subject shall have the right to obtain from the controller the erasure of personal data concerning him or her without undue delay and the controller shall have the obligation to erase personal data without undue delay under some grounds. Off-chain storage technology can help the blockchain industry comply with GDPR rules, allowing offline storage of personal data, or allow trusted nodes to delete the private key of encrypted information, which leaving data that cannot be read and identified on the chain. If the data is in accordance with the definition of anonymization by GDPR, there is no room for GDPR to be applied. IV. Conclusion In summary, it’s seem that the application of blockchain to GDPR may include: (a) being difficulty to identified the data controllers and data processors after the data subject upload their data. (b) the nature of decentralized storage is transnational storage, and Whether the country where the node is located, is meets the “adequacy decision” of Article 45 of the GDPR. If it cannot be met, then it needs to consider whether it conforms to the transfers subject to appropriate safeguards of Article 46, or the derogations for specific situations of Article 49 of the GDPR. Reference: [1] How to Trade Cryptocurrency: A Guide for (Future) Millionaires, https://wikijob.com/trading/cryptocurrency/how-to-trade-cryptocurrency [2] DONNA K. HAMMAKER, HEALTH RECORDS AND THE LAW 392 (5TH ED. 2018). [3] Iansiti, Marco, and Karim R. Lakhani, The Truth about Blockchain, Harvard Business Review 95, no. 1 (January-February 2017): 118-125, available at https://hbr.org/2017/01/the-truth-about-blockchain [4] Article 29 Data Protection Working Party, Opinion 05/2014 on Anonymisation Techniques (2014), https://www.pdpjournals.com/docs/88197.pdf [5] Directive 95/46/EC (General Data Protection Regulation), https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:32016R0679&from=EN [6] Queen Mary University of London, Are blockchains compatible with data privacy law? https://www.qmul.ac.uk/media/news/2018/hss/are-blockchains-compatible-with-data-privacy-law.html

Introduction to Tax Incentive Regime for SMEsIntroduction to Tax Incentive Regime for SMEs I. Introduction The developments of SMEs (small-and-medium enterprises) plays an important pillar of development of industries and creation of jobs in Taiwan. In 2017, the total number of SMEs in Taiwan was 1,437,616. They offer 8,904,000 jobs, accounting for 78.44% of the workforce[1]. However, SMEs have difficulties in entering international supply chains because of their weakness in finance. Therefore, how to enhance the global competitiveness of SMEs is an important issue for the concerned authority. Chapter 4 of the Act for Development of Small and Medium Enterprises prescribes the tax incentive regime based on the financial capability of SMEs and characteristics of industries in order to facilitate the development of SMEs, especially the globalization of SMEs. This paper will review the importance of tax incentives to SMEs and introduces the tax incentive regime under the Act for Development of Small and Medium Enterprises In order to help SMES have an understanding of such regime. II. SME Tax Incentives Scheme As the gatekeeper of the market, the government may intervene the market with various policies or tools to reallocate and improve the soundness of the market environment when the market competitions is impaired due to information asymmetry or externalities. At this juncture, preferential tax rates or tax deductions can be offered to specific taxpayers through legal institution. This allows these taxpayers to retain higher post-tax earnings so that they are incentified to invest more resources in the legally defined economic activities. Tax incentives targeting at risky or spillover investments to create benefits to specific economic activities will help the development of industries and markets. Whilst Article 10 of the Statute for Industrial Innovation has provided tax cuts for R&D expenditures, these incentives are not focus on SMEs and hence not supportive to their research and innovations. This was the reason for the 2016 amendment of the Act for Development of Small and Medium Enterprises added Article 35 to offer tax incentives in order to encourage R&D and innovative efforts and Article 35-1 to activate intellectual properties via licensing. These articles aim to accelerate the momentum of innovations and transformations which promoting investments for SMEs. OthersTo assist SMEs to cope with change of the business environment, the Article 36-2 added the tax incentives for salary or headcount increases, to contribute to the sustainability of SMEs and stabilize the labour market and industrial structures. Following is an explanation of the applicability of these schemes and the requirements to qualify such incentives. III. Tax Incentives to Promote Investments (I) Tax deductions for R&D expenditures Governments around the world seek to encourage corporate R&D activities, that Tax incentives are put in place to reduce R&D costs and foster a healthy environment of investment for more R&D initiatives. Neighboring countries such as Japan, Korea and Singapore are frequently practicing belowing tax burdens to encourage R&D efforts. Article 35 of the Act for Development of Small and Medium Enterprises in Taiwan allows accelerated depreciation and offers tax cuts[2] to stimulate R&D and innovations and create an investment friendly environment for SMEs. 1. Taxpaying Entities and Requirements (1) Qualifications for SMEs Article 35 of the Act is applicable to qualified SMEs and individual taxpayers, which are (1) from manufacturing, construction & engineering, mining and quarrying industries, with paid-in capital below or equal to NT$80 million or with the number of full-time employees less than 200 people; (2) from other industries with the sales of the previous year below or equal to NT$100 million or with the number of full-time employees less than 100 people. Thus, the qualifications of Small and Medium Enterprises are based on either paid-in capital/sales or number of employees under the Act[3].Meanwhile, SMEs may not have an independent R&D department due to the limit of size or operating cost.Therefore, if the taxpayers hiring full-time R&D personnel that can provide records of job descriptions and work logs to R&D activities, the SMEs can access the tax incentives provided that the R&D functions. The recognized by government agencies is increasingly flexibility for SMEs seeking policy support. 2. Taxpayers and requirements (1) A certain degree of innovativeness As the tax incentive regime strives to promote innovations, the R&D expenses should be used to fund innovative developments. According to the official letters from the Small and Medium Enterprise Administration, Ministry of Economic Affairs, there is no high bar as forward-looking, risky and innovative as usually” required for other incentives previously, which is considering the size of SMEs and their industry characteristics. The “certain degree” of innovativeness shall be based on industry environments and SME businesses as determined by competent authorities in a flexible manner. (2) Flexibility in the utilization of business income tax reductions To encourage regular R&D activities, The case that SMEs may not have R&D undertakings each year due to funding constraints, or start-up company may have incurred R&D expenditures but are not yet profitable and hence have no tax liabilities during the year, Corporate taxpayers were able to choose beside deduct the payable taxes during a single year, and reduce the payable taxes during the current year over three years starting from the year when tax incentives are applicable. 3. Tax incentive effects As previously mentioned, Article 35 of the Act for Development of Small and Medium Enterprises accommodates the characteristics of SMEs by allowing reductions of corporate business taxes for up to 15% R&D expenditures during the current year, or spreading the tax reductions by spreading up to 10% of the R&D expenditures over three years from the first year when the incentives are applicable. It is worth noting that the tax deductions shall not exceed 30% of the payable business income taxes during a single year. If the instruments and equipment for R&D, experiments or quality inspections have a lifetime over two years or longer, it is possible to accelerate the depreciation within half of the years of service prescribed by the income tax codes for fixed assets. However, the final year less than 12 months over the shortened service years shall not be counted. Accelerated depreciation brings in tax benefits for fixed asset investments during the initial stage, that meets the requirements for new technologies and risk management by frontloading the equipment depreciation and creates a buffer for capital utilization. (II) Deferred taxations on licensing/capitalization of intellectual properties The deferral of tax payments under the Act for Development of Small and Medium Enterprises is meant to avoid any adverse effect on the application of technological R&Ds by SMEs. As the equity stakes via capitalization of intellectual properties by inventors or creators are not cashed out yet and the subsequent gains may not be at the same valuation as determined at the time of capitalization, the immediate taxation may hinder the willingness to transfer intellectual properties. Therefore, assisting SMEs to release intellectual properties with potential economic value, the licensing and capitalization of intellectual properties is strongly encouraged. The tax expenses shall be deferred within SME or an individual acquires stakes on a non-publicly-listed company by transferring their intellectual properties. This is to stimulate the applications and sharing of relevant manufacturing technologies. When an SME or an individual acquires stakes on a non-publicly-listed company by transferring their intellectual properties, their tax expenses shall be deferred. 1. Taxpayers and requirements (1) Qualifications for individuals or SMEs Article 35-1 of the Act for Development of Small and Medium Enterprises is applicable to SMEs and individual taxpayers. This is to foster the growth of SMEs and enhancement of industry competitiveness by encouraging R&D and innovations from individuals and start-ups. To promote the commercialize of intellectual properties in different ways, the Act for Development of Small and Medium Enterprises provides income tax incentives to individuals and SMEs transferring intellectual properties. The purpose is to encourage different paths to industry upgrades. (2) Ownership of intellectual properties To ensure that the proceeds of intellectual property is linked to the activity of intellectual properties which perform by individuals or SMEs. Only the owners of the intellectual properties capitalized and transferred can enjoy the tax benefits. Intellectual properties referred to in the Act for Development of Small and Medium Enterprises are the properties with value created with human activities and hence conferred with legal rights. These include but are not limited to copyrights, patent rights, trademarks, trade secrets, integrated circuit layouts, plant variety rights and any other intellectual properties protected by laws[4]. (3) Acquisition of stock options The abovementioned tax incentives are offered to the individuals or SMEs who transfer intellectual properties to non-listed companies in exchange of their new shares. The income taxes on the owners of intellectual properties are deferred until acquisition of shares. These shares are not registered with the book-entry system yet. Before the transferrers of intellectual properties dispose or offload these shares, immediate taxations will impose economic burdens and funding challenges given the unknown prices of the eventual cash-out. Therefore, this legislation is only applicable to taxpayers who obtain options for new shares. 2. Taxpayers and requirements (1) Transfer of intellectual properties According to Article 36 of the Copyright Act as interpreted by official letters issued by the Ministry of Finance, the transfer of intellectual properties is the conferring of intellectual properties to others, and the transferees access these intellectual properties within the scope of the transfer. In terms “transfer” of the first and second paragraphs of Article 36 does not include licensing[5], but such as granting, licensing and inheritance. (2) Timing of income tax payments In general, the particular time that calculation of taxes payable is based on when the taxpayers acquire the incomes, less relevant expenses or costs. The taxes payable timing should be depending on when the taxpayers obtain the newly issued shares by transferring intellectual properties. However, the levy of income taxes at the time of intellectual property transfers and new share acquisitions may cause a sudden jump in taxes payable in the progressive system and thus a burden on the economics of SMEs and individuals concerned. Thus, to avoid disruptions to company operations or personal finance planning, Article 36 makes the exception for the incomes earned by subscribing to new shares as a result of transferring intellectual properties. Such incomes are not subject to taxes during the year when the shares are acquired, in order to mitigate the tax barriers concerned. In sum, the taxes shall be paid when such shares are transferred, gifted or distributed. 3. Tax incentive effects Article 35-1 of the Act for Development of Small and Medium Enterprises provides tax incentives to stimulate the mobilization of intellectual properties by smoothing out the impact of income taxes payable. This is applicable to (1) SMEs who can postpone the business income taxes payable from the year when they acquire new shares of non-listed companies by transferring the intellectual properties they own; (2) individuals who can postpone the individual income taxes payable from the year when they acquire new shares of non-listed companies by transferring the intellectual properties they own. IV. Tax incentives aiming to improve the business environment (I) Tax reductions for wages to additional headcounts SMEs are vital to the Taiwan, making uo 90% of the companies accounting in Taiwan, who employ more than 6.5 million people or 72.8% of the total workforce. Any economic recession may make it difficult for SMEs to maintain their labor costs given their smaller funding size and external challenges. This will cause higher unemployment rates and hurt the economy, which may cause impairment of the capacity or create a labor gap for SMEs, eventually shrink the industry scale. To lower the burden of operational and investment costs and learn from the legislatives in Japan and the U.S.[6], tax incentives are put in place as a buffer for adverse effects of external environments. The first paragraph of Article 36-2 of the Act for Development of Small and Medium Enterprises provide tax incentives for employee salaries of new headcounts based on the assessment on the economy over a time period. This is intended to encourage domestic investments and avoid the pitfall of direct government subsidies distorting salary structures. It is hoped that investments from SMEs can stimulate the momentum of economic growth. 1. Taxpayers The tax incentives under Article 36-2 of the Act for Development of Small and Medium Enterprises aim to assist SMEs through difficult times in an economic downturn. The threshold of the period time is based on the unemployment rate has been below the economic indicator predetermined for six consecutive months, which calculated by the Directorate General of Budget, Accounting and Statistics, Executive Yuan. In number of the unemployment rate has been below the economic indicator predetermined for six consecutive months, it is deemed that the business environment is not friendly to SMEs. In this instance, the Regulations for the Tax Preferences Provided to Small and Medium-sized Enterprises on Additional Wage Payment will trigger the tax incentives. The abovementioned economic indicator shall be published by the competent authorities once every two years. Moreover, to qualify for the tax incentives for new employees, SMEs should investing new ventures or instill new capital by at least $500,000[7] or hiring workforce at least two full-time headcounts compared with the previous fiscal year, that constitute at the Article 36-2 of the Act for Development of Small and Medium Enterprises, which aims to encourage SMEs investments. 2. Taxpayers (1) Qualifications of additional headcounts As the dispatched human resource services typically meet temporary or short-term requirements and contractors do not enjoy employment security, this is not consistent with the spirit of the legislation to create jobs and reduce unemployment. Therefore, to avoid the one-time increase of headcounts from accessing the tax reductions during the year and the deterioration of labor relations in Taiwan. Tax incentive is not offered to the additional recruitment of part-time or contracted workers. Meanwhile, the tax incentives are only applicable to the additional employment of Taiwanese nationals, above or below 24 years old. A tax deduction of 50% based on annual wages is provided for the hiring of people below 24 years old. The extra tax deduction will stimulate young employment. (2) Definition of additional employment The number of additional headcounts is based on permanent hires and calculated as the difference between the average number of Taiwanese employees covered by labor insurance per month throughout a single fiscal year or before and after the incremental increase of workforce. The conversion of regular contracts to indefinite employment in writing or signing up for indefinite R&D headcounts under the military service scheme can also be deemed as additional employment. It is worth noting, however, the new headcounts resulted from M&A activities or transfer between affiliated companies are excluded in this legislation. (3) Calculation of wages Companies are also required to increase employment as well as the Comparable Wages. The comparable wages are estimated with the summation of 30% of the wages for the year before and after additional employment that based on the aggregate of the new hires comparable wages compared to the prior year. In other words, if the aggregate wages paid out are higher than comparable wages during the year, the companies concerned have indeed incurred higher personnel expenses. Tax incentives are thus granted because it improves the business environment and it is the purpose of this legislation. 3. Tax incentive effects The first paragraph of Article 36-2 of the Act for Development of Small and Medium Enterprises provides deductions of business income taxes during the year to qualified SMEs at an amount equivalent to 130% of the incremental wages paid to new headcounts who are Taiwanese nationals. The deductible amount is equivalent to 150% of the incremental wages if new headcounts are Taiwanese nationals below 24 years old. (II) Tax incentives for companies that increase salaries Companies are subject to the effect of changes in the external factors such as global supply and demand on the international market, as well as the domestic business environment as a result of risk aversion from investors and expectation from customers. These uncertainties associated with investments and the rising prices for consumers will suppress the wage levels in Taiwan. This the reason why the second paragraph of Article 36-2 of the Act for Development of Small and Medium Enterprises grants tax deductions for the companies who increase salaries, to encourage companies share earnings with employees and enhance private-sector consumption. SMEs may deduct their business income taxes payable during the year up to 30% of salary increase for existing entry-level employees who are Taiwanese nationals, not as a result of statutory requirement for basic wage adjustments. 1. Taxpayers The tax incentives are applicable to SMEs as defined by the Regulations for the Tax Preferences Provided to Small and Medium-sized Enterprises on Additional Wage Payment and based on the same economic indicators previously mentioned. 2. Qualification for tax incentives (1) Definition of entry-level employees The object of taxation under this act is the enterprise's average wage payment to the entry-level employees. The entry-level employees referred to in this act are authorized by the "Small and medium-sized enterprise employee salary increase, salary deduction act " that refers to employees of local nationality with an average monthly recurring salary below nt $50,000[8] whose were entered into indefinite employment contracts with SMEs. Through such conditions, the effect of tax concessions will be concentrated on promoting the salary level of grassroots staff and helping enterprises to cope with changes in the industrial environment. (2) Average salaries The salaries to entry-level employees refer to the basic salaries, fixed allowances and bonuses paid on a monthly basis. Payment-in-kind shall be discounted based on the actual prices and included into the regular salaries. Meanwhile, regular salaries should be calculated with annualized averages, as this legislation seeks to boost salary levels. The regular salaries to entry-level employees during the year are estimated with the monthly number of entry-level employees during the same year. Only when the average basis salaries during the year are higher than those in the prior year can the tax incentives be applicable. 3. Tax incentive effects Applying this article, SMEs can deduct their business income taxes each year up to 130% of salary increase for existing entry-level employees who are Taiwanese nationals, which are not as a result of statutory requirement for basic wage adjustments. However, it is not allowed to double count the increased personnel expenses for new headcounts applicable to the first and second paragraphs of the same article. V. Conclusions The funding scales and relatively weak financial structures are the factors that led SMEs be susceptible influenced by supply change dynamics and business cycles. To the extent that is suppressing the flexible in capital utilization for SMEs, also influencing on the sustainability of SMEs. Differ from government subsidies require budgeting, reviewing and implementations, there are complications regarding the allocation of administrative resources. Therefore, it is important to plan for tax incentives in order to stimulate R&D, innovation and job creation by SMEs and ultimately make SMEs more competitive. The tax incentives to SMEs amended in 2016 by the Small and Medium Enterprise Administration are known for the following: (I) The lowering of thresholds for tax reductions of R&D expenses in order to encourage SMEs to invest in R&D activities with a “certain degree” of innovativeness and enhance the momentum for SMEs to upgrade and transform themselves; (II) Deferral the income taxations on the transfer of intellectual properties for equity, in order to encourage application and utilization of such intellectual properties, provide incentives for R&D programs or innovations by individuals and SMEs. This also creates a catalyst for industry upgrade; (III) Tax deductions for the employment of new headcounts or the increase of employee wages during the time the economic indicators have reached a certain threshold and based on the health of the investment environment. This is to encourage company investments and capital increases in Taiwan and mitigate the volatility of economic cycles, in order to get ready for business improvement. The above tax incentive programs, i.e. tax deductions for R&D and innovations; deferral of taxations on the transfer of intellectual properties for equity; tax deductions for the hiring of new headcounts and the increase of employee salaries, are meant to boost the investment from SMEs and the competitiveness of SMEs. The Act for Development of Small and Medium Enterprises seeks to reduce tax burdens of SMEs actively investing for their future and competitive advantages. Tax incentives help to mitigate the adverse effect of the economy on the business environment. It is also the fostering of the sources of business income tax revenues for the government. This is the very purpose of the Act for Development of Small and Medium Enterprises. [1]White Paper on Small and Medium Enterprises in Taiwan, 2018, p21 (November 9, 2018) published by the Ministry of Economic Affairs [2]Pursuant to the authorization conferred by Article 35 of the Act for Development of Small and Medium Enterprises, the Ministry of Economic Affairs has announced the Regulations Governing the Reduction of Expenditures for Small and Medium Enterprises Research and Development as Investment. [3]Article 2 on the definition of SMEs. The abovementioned criterion is universally applicable to the Act for Development of Small and Medium Enterprises. It also applies to the eligibility of tax incentives to be introduced in this paper unless otherwise specified. [4]Official Letter Economic-Business No. 10304605790, Ministry of Economic Affairs [5]Official Letter Taiwan-Finance No. 10300207480, Ministry of Finance [6]“Assessment of the Taxations under Article 35, Article 35-1, the first paragraph and the second paragraph of Article 36-2, the Act for Development of Small and Medium Enterprises” published by the Small and Medium Enterprise Administration, Ministry of Economic Affairs, pages 15-17, https://www.moeasmea.gov.tw/files/2670/93B9AF54-84E2-4293-A5CA-EA7DD9FAA05A(most recently browsed date September 9, 2019). [7]Order of Interpretation Economics-Business No. 104004602510 from the Ministry of Economic Affairs: “Second, on the day when the economic indicator has reached the threshold, the paid-in capital of the new business should be at least NT$500,000 and there is no need to instill additional capital during the period when tax incentives are applicable. For existing businesses, there is no limitation on the number of capital increases during the applicable period. So long as the cumulative increase in capital reaches NT$500,000 and new employees are hired during the same fiscal year or during the prior fiscal year.” [8]Paragraph 1, Article 2 of the Regulations for the Tax Preferences Provided to Small and Medium-sized Enterprises on Additional Wage Payment

Brief Introduction to Taiwan Social Innovation PoliciesBrief Introduction to Taiwan Social Innovation Policies 2021/09/13 1. Introduction The Millennium Development Goals (MDGs)[1] set forth by the United Nations in 2000 are carried out primarily by nations and international organizations. Subsequently, the Sustainable Development Goals (SDGs) set forth by the United Nations in 2015 started to delegate the functions to organizations of all levels. Presently, there is a global awareness of the importance of balancing “economic growth”, “social progress”, and “environmental protection” simultaneously during development. In the above context, many similar concepts have arisen worldwide, including social/solidarity economy, social entrepreneurship and social enterprise, and social innovation. Generally, social innovation aims to alter the interactions between various groups in society through innovative applications of technology or business models, and to find new ways to solve social problems through such alterations. In other words, the goal is to use innovative methods to solve social problems.The difference between social innovation and social enterprise is that social enterprise combines commercial power to achieve its social mission under a specific perspective, while social innovation creates social value through cooperation with and coordination among technology, resources, and communities under a diversified nature. 2. Overview of Taiwan Social Enterprise Policy To integrate into the global community and assist in the development of domestic social innovation, Taiwan’s Executive Yuan launched the “Social Enterprise Action Plan” in 2014, which is the first policy initiative to support social enterprises (from 2014 to 2016).Under this policy initiative, through consulting with various ministries and applying methods such as “amending regulations”, “building platforms”, and “raising funds”, the initiative set to create an environment with favorable conditions for social innovation and start-ups. At this stage, the initiative was adopted under the principle of “administrative guidance before legislation” in order to encourage private enterprise development without excessive burden, and avoid regulations restricting the development of social enterprises, such as excessive definition of social enterprises. Moreover, for preserving the original types of these enterprises, this Action Plan did not limit the types of social enterprises to companies, non-profit organizations, or other specific types of organizations. To sustain the purpose of the Social Enterprise Action Plan and to echo and reflect the 17 sustainable development goals proposed in SDGs by the United Nations, the Executive Yuan launched the “Social Innovation Action Plan” (effective from 2018 to 2022) in 2018 to establish a friendly development environment for social innovation and to develop diversified social innovation models through the concept of “openness, gathering, practicality, and sustainability”.In this Action Plan, “social innovation” referred to “social innovation organizations” that solve social problems through technology or innovative business models. The balancing of the three managerial goals of society, environment value, and profitability is the best demonstration of the concept of social innovation. 3. Government’s Relevant Social Enterprise Policy and Resources The ministries of the Taiwan Government have been promoting relevant policies in accordance with the Social Innovation Action Plan issued by the Executive Yuan in 2018, such as the “Registration System for Social Innovation Enterprises” (counseling of social enterprises), the “Buying Power - Social Innovation Products and Services Procurement”, the “Social Innovation Platform” established by the Ministry of Economic Affairs, the “Social Innovation Manager Training Courses”, the “Promoting Social Innovation and Employment Opportunities” administered by the Ministry of Labor, and the “University Social Responsibility Program” published by the Ministry of Education. Among the above policies stands out the measures adopted by the Ministry of Economic Affairs, and a brief introduction of those policies are as follows: i. Social Innovation Platform To connect all resources involved in social issues to promote social innovation development in Taiwan, the Ministry of Economic Affairs established the “Social Innovation Platform”.[2] With visibility through the Social Innovation Platform, it has become more efficient to search for targets in a public and transparent way and to assist with the input of resources originally belonging to different fields in order to expand social influence. As a digital platform gathering “social innovation issues in Taiwan,” the Social Innovation Platform covers multiple and complete social innovation resources, which include the “SDGs Map” constructed on the Social Innovation Platform, by which we can better understand how county and city governments in Taiwan implement SDGs and Voluntary Local Review Reports, and which allow us to search the Social Innovation Database[3] and the registered organizations, by which citizens, enterprises, organizations, and even local governments concerned with local development can find their partners expediently as possible, establish service lines to proactively assist public or private entities with their needs/resources, and continue to enable the regional revitalization organizations, ministries, and enterprises to identify and put forward their needs for social innovation through the function of “Social Innovation Proposals”, which assist social innovation organizations with visibility while advancing cooperation and expanding social influence. In addition, the “Event Page” was established on the Social Innovation Platform and offers functions, such as the publishing, searching, and sorting of events in four major dimensions with respect to social innovation organization, governments, enterprises, and citizens; and encourages citizens, social innovation organizations, enterprises, and governments to devote themselves via open participation to continuously expande the influence of the (Civic Technology) Social Innovation Platform. The “Corporate Social Responsibility Report” collects the corporate social responsibility reports, observes the distribution of resources for sustainable development by corporations in Taiwan, offers filtering functions by regions, keyword, popular rankings, and or SDGs types, and provides contact information and a download function for previous years’ reports, in order to effectively assist social innovation organizations to obtain a more precise understanding of the status quo, needs, and trends with respect to their development of respective products and services. Figure 1: SDGs Map Reference: Social Innovation Platform (https://si.taiwan.gov.tw/) Figure 2: Social Innovation Database Reference: Social Innovation Platform (https://si.taiwan.gov.tw/) Figure 3: Social Innovation Proposals Reference: Social Innovation Platform (https://si.taiwan.gov.tw/) Figure 4: Event Page Reference: Social Innovation Platform (https://si.taiwan.gov.tw/) Figure 5: Corporate Social Responsibility Report Reference: Social Innovation Platform (https://si.taiwan.gov.tw/) ii. Social Innovation Database To encourage social innovation organizations to disclose their social missions, products and services, and to guide society to understand the content of social innovation, and to assist the administrative ministries to be able to utilize such information, the Ministry of Economic Affairs issued the “Principles of Registration of Social Innovation Organizations” to establish the “Social Innovation Database”. Once a social innovation organization discloses the items, such as its social missions, business model, or social influence, it may obtain the relevant promotional assistance resources, including becoming a trade partner with Buying Power (Social Innovation Products and Services Procurement), receiving exclusive consultation and assistance from professionals for social innovation organizations, and becoming qualified to apply to entering into the Social Innovation Lab.Moreover, the Ministry of Economic Affairs is simultaneously consolidating, identifying, and designating the awards and grants offered by the various ministries, policies and measures in respect of investment, and financing and assistance, as resources made available to registered entities. As of 25 May 2021, there were 658 registered social innovation organizations and 96 Social Innovation Partners (enterprises with CSR or ESG resources that recognize the cooperation with social innovation under the social innovation thinking model may be registered as a “Social Innovation Partner”).The public and enterprises can search for organizations registered in the Social Innovation Database through the above-said Social Innovation Platform, the search ability of which advances the exposure of and the opportunities for cooperation with social innovation organizations. Figure 6: Numbers of registered social innovation organizations and accumulated value of purchases under Buying Power Reference: Social Innovation Platform(https://si.taiwan.gov.tw/) iii. Buying Power - Social Innovation Products and Services Procurement In order to continue increasing the awareness on social innovation organizations and related issues and promote responsible consumption and production in Taiwan, as well as to raise the attention of the commercial sector to the sustainability-driven procurement models, the Ministry of Economic Affairs held the first “Buying Power - Social Innovation Products and Services Procurement” event in 2017. Through the award system under the Buying Power, it continues to encourage the governments, state-owned enterprises, private enterprises, and organizations to take the lead in purchasing products or services from social innovation organizations, to provide the relevant resources so as to assist social innovation organizations to obtain resources and to explore business opportunities in the markets, to practice responsible consumption and production, and to promote innovative cooperation between all industries and commerce and social innovation organizations. The aim of the implementation of the Buying Power is to encourage the central and local governments, state-owned enterprises, private enterprises, and non-governmental organizations to purchase products or services from organizations registered in the Social Innovation Database, while prizes will be awarded based on the purchase amounts accumulated during the calculation period. The winners can obtain priority in applying for membership in the Social Innovation Partner Group, with corresponding member services, in the future. Under the Social Innovation Platform, both the amount of purchase awards and the number of applicants for special awards continue to increase.So far, purchases have accumulated to a value of more than NT$1.1 billion (see Figure 6), and more than 300 organizations have proactively participated. iv. Social Innovation Mark In order to promote public awareness of social innovation, the Ministry of Economic Affairs has been charged with the commissioned task of promoting the Social Innovation Mark, and issued “ The Small and Medium Enterprise Administration of the Ministry of Economic Affairs Directions for Authorization of the Social Innovation Mark” as the standard for the authorization of the Social Innovation Mark. Social innovation organizations can use the Mark, through obtaining authorization, to hold Social Innovation Summits or other social innovation activities for promoting social innovation concepts. In order to build the Mark as a conceptual symbol of social innovation, the Ministry of Economic Affairs has been using the Social Innovation Mark in connection with various social innovation activities, such as the Social Innovation Platform, the Buying Power, and the annual Social Innovation Summit. Taking the selection of sponsors of the Social Innovation Summit in 2022 as an example[4], only organizations that have obtained authorization of the Social Innovation Mark can use the Mark to hold the Social Innovation Summit. Figure 7: The Social Innovation Mark of the Small and Medium Enterprise Administration, Ministry of Economic Affairs IV. Conclusion The “Organization for Economic Cooperation and Development” (OECD) regards social innovation as a new strategy for solving future social problems and as an important method for youth entrepreneurship and social enterprise development.Taiwan’s social innovation energy has entered a stage of expansion and development. Through the promotion of the “Social Innovation Action Plan,” the resources from the central and local governments are integrated to establish the Social Innovation Platform, the Social Innovation Database, the Social Innovation Lab, and the Social Innovation Mark. In addition, incentives such as the Buying Power have been created, manifesting the positive influence of Taiwan’s social innovation. [1] MDGs are put forward by the United Nations in 2000, and are also the goals requiring all the 191 member states and at least 22 international organizations of the United Nations to be committed to on their best endeavors, including: 1. eradicating extreme poverty and hunger, 2. applying universal primary education, 3. promoting gender equality and empowering women, 4. reducing child mortality rates, 5. improving maternal health, 6. combatting HIV/AIDS, malaria, and other diseases, 7. ensuring environmental sustainability, and 8. establishing a global partnership for development. [2] Please refer to the Social Innovation Platform: https://si.taiwan.gov.tw/. [3] Please refer to the Social Innovation Database: https://si.taiwan.gov.tw/Home/Org_list. [4] Please refer to the guidelines for the selection of sponsors of the 2022 Social Innovation Summit: https://www.moeasmea.gov.tw/files/6221/4753E497-B422-4303-A8D4-35AE0B4043A9

Innovative Practice of Israel's Government ProcurementInnovative Practice of Israel's Government Procurement Government procurement is an important pillar of government services. Because of the huge number of government purchases, government procurement management play an important role in promoting public sector efficiency and building citizenship. Well-designed government procurement systems also help to achieve policy such as environmental protection, innovation, start-ups and the development of small and medium-sized enterprises. Nowadays, countries in the world, especially OECD countries, have been widely practiced with innovative procurement to stimulate innovation and start-ups, and call Innovation procurement can deliver solutions to challenges of public interest and ICTs can play a major role in this. However, in the OECD countries, in addition to the advanced countries that have been developed, many developing countries have also used government procurement to stimulate national R & D and innovation with remarkable results. Israel is one of the world's leading technology innovation centers, one of the most innovative economies in the world, continues to leverage its own strengths, support of technology entrepreneurship and unique environment, an international reputation in the high-tech industry, the spirit of technological innovation and novelty. Government procurement is a core element of the activities of Israeli government, agreement with suppliers and compliance with the Mandatory Tenders Law. The main challenge is how to ensure efficiency and maintain government performance while ensuring an equitable and transparent procurement process. Israel’s Mandatory Tenders Law has shown the central role played by the Israeli Supreme Court in creating and developing this law, even in the absence of any procurement legislation, based instead on general principles of administrative law. Once the project of creating a detailed body of public tendering law had been completed, and the legislator was about to step in, the Supreme Court was prepared to step out and transferring the jurisdiction to lower courts. The Knesset passed the Mandatory Tenders Law, and based on it the Government issued the various tendering regulations. Besides, Israel's various international agreements on government procurement, mainly GPA and other bilateral international agreements such as free trade agreements with Mexico and Colombia and free trade agreements and memoranda of understanding with the United States. The practical significance of these commitments can only be understood on the backdrop of Israel’s domestic preference and offset policies. These policies were therefore discussed and analyzed as they apply when none of the international agreements applies. The Challenge Tenders "How to solve the problem of overcrowding in the emergency department and the internal medicine department?" is the first of a series of "problem solicitations" released by the Israeli Ministry of Health which seeks to find a digital solution to the public health system problem, questions from the government while avoiding preconceived prejudices affect the nature of the solution, allowing multiple innovative ideas from different fields to enter the health system, make fair and transparent judgments about the ideal solution to the problem. In order to ensure transparency and integrity, equality, efficiency and competition in the decision-making process, the tender proposed by the Israeli Ministry of Health defines a two-stage tender process. The Ministry of Health of Israel, in order to improve the quality of medical care, shorten the waiting time for hospitalized patients, protect the dignity of patients and their families with patients as its center, and ensure their rights, while alleviating the burden of hospital staff, so as to pass the targeted treatment areas reduce the gap between various residential areas. The Israeli government deals with these issues through challenging tenders and offers a digital solution combined with innovative ideas. The initiative proposed through the development of public service projects can raise the level of public services in the country and help the government to reduce costs and achieve the purpose of promoting innovation with limited conceptual, technical and financial capabilities. In addition, due to the online operation of the challenging tender process throughout the entire process, fair and transparent procedures can be ensured, while public-private partnerships are encouraged to facilitate the implementation of the implementation plan.

- Impact of Government Organizational Reform to Scientific Research Legal System and Response Thereto (1) – For Example, The Finnish Innovation Fund (“SITRA”)

- The Demand of Intellectual Property Management for Taiwanese Enterprises

- Blockchain in Intellectual Property Protection

- Impact of Government Organizational Reform to Research Legal System and Response Thereto (2) – Observation of the Swiss Research Innovation System

- Recent Federal Decisions and Emerging Trends in U.S. Defend Trade Secrets Act Litigation

- The effective and innovative way to use the spectrum: focus on the development of the "interleaved/white space"

- Copyright Ownership for Outputs by Artificial Intelligence

- Impact of Government Organizational Reform to Research Legal System and Response Thereto (2) – Observation of the Swiss Research Innovation System